The Benefits of Avoiding Tax Refunds: Why You Shouldn't Receive One

As tax season approaches, many individuals anticipate receiving a tax refund and contemplate how to utilize it wisely. While conventional advice often suggests putting the refund towards a mortgage, adding it to an RRSP, or making a TFSA contribution, we propose an alternative approach: not receiving a tax refund at all.

At first glance, this might seem counterintuitive. After all, isn't it beneficial to receive a substantial tax refund that can be used in various ways? However, let's explore why it's advantageous to forgo a tax refund and instead receive additional money in your regular paycheques throughout the year. We'll also delve into methods to reduce at-source tax deductions and how to allocate the extra funds.

Why do people receive tax refunds?

To understand why individuals receive tax refunds, we need to consider that most employed individuals have taxes deducted at source. This means that the money received in their paycheques has already undergone tax deductions, along with CPP and EI contributions, facilitated by their company's payroll department. However, these deductions often fail to account for common expenses that can be claimed on tax returns to lower the tax owed. Such expenses include personal RRSP contributions unrelated to work, child-care expenses, spousal support, and charitable donations. If substantial amounts are spent on these items, a sizable tax refund may be expected.

Why is it better to forego a tax refund?

Receiving a significant tax refund can be viewed as inefficient tax planning. Throughout the year, you end up paying more in taxes than necessary, and that money remains with the Canada Revenue Agency, generating interest for the government instead of contributing to your own financial plans. Moreover, depending on when you file your taxes, it may take up to 16 months before you receive that money.

Let's consider an example: Suppose you receive a tax refund of $5,040 on May 1 for your previous year's tax contributions. While this is undoubtedly a substantial windfall that could make a significant contribution towards your savings goals, what if you received an extra $420 in your monthly paycheques instead of a large tax refund?

Assuming you invested this additional money and earned a 5% return, by the following May 1, your initial capital of $5,040 would have grown to $5,243, an additional $203. Now, imagine the potential growth of your investments over 10, 20, or even 30 years, where the power of compound returns comes into play. By allowing that money to work for you sooner, you can expedite the achievement of your financial objectives.

How to reduce at-source tax deductions

Reducing your payroll deductions is a relatively straightforward process. To reduce tax deductions at the source, you must fill out the T1213 Request to Reduce Tax Deductions at Source form provided by the Government of Canada and submit it to your nearest CRA tax center. You can find the location of your nearest center by visiting this link.

Upon approval, the government will authorize a reduction in your withholdings, which you should forward to your employer's payroll department. Depending on the amount, you could witness a substantial increase in your take-home pay. While this process can be initiated at any time during the year, it is advisable to do so as early as possible.

What should you do with the extra money in your paycheque?

While many financial institutions often recommend putting your tax refund towards an RRSP or using it to pay down your mortgage, the optimal utilization of the additional funds will vary from person to person. Let's explore some potential options:

1. Increasing your RRSP contributions: If you need to bolster your retirement savings, increasing your RRSP contributions can be a suitable choice. The longer you save, the more you benefit from tax-deferred growth, and your contributions will immediately reduce your taxable income. Ensure that you have sufficient contribution room to avoid overcontribution penalties.

2. Maximizing your Tax-Free Savings Account (TFSA): The TFSA contribution limit increased to $6,500 in 2023. If you meet the eligibility criteria and have not yet contributed to a TFSA, you can contribute up to $88,000 this year. While TFSA contributions are not tax deductible, the account offers tax-free growth (including interest, capital gains, and dividends), and funds can be withdrawn at any time without penalty or tax. The TFSA provides flexibility and should be incorporated into everyone's financial plan.

3. Growing a Registered Education Savings Plan (RESP): If you have children and wish to save for their post-secondary education, an RESP is an ideal option. You have the opportunity to receive government grants of up to $7,200 throughout your lifetime, and the savings will grow tax-deferred. Explore the benefits of RESPs to understand the advantages further.

4. Building an emergency fund: If you lack an emergency fund, consider allocating some of the extra money towards establishing one. An emergency fund acts as a safety net, protecting your financial plans from unexpected large expenses. Your TFSA can serve as an excellent place to store some or all of your emergency funds.

5. Paying off high-interest debt: If you carry balances on credit cards or high-interest lines of credit, it is advisable to prioritize paying off these debts before considering other options. The interest you pay on these debts typically exceeds the potential investment returns, making debt repayment a wise decision.

6. Accelerating mortgage payments: For individuals with a priority of becoming mortgage-free as soon as possible, paying off the mortgage faster might be appealing. However, if your mortgage interest rate is significantly lower than the after-tax returns you could earn from investments, it may be prudent to explore alternative strategies.

7. Heading Vegas and wagering everything on red: Just kidding! Put it all on black. Still kidding. Don't go to Vegas.

Before making any decisions, consult your advisor. Don’t have an advisor? Contact me and my team!

Having extra money to save every month is always advantageous, regardless of your financial plan or goals. However, it is crucial to determine the best use of those funds based on your unique circumstances. We can evaluate your overall financial situation and provide personalized guidance on the most effective utilization of the money for both short-term and long-term objectives.

Jun 02, 2023

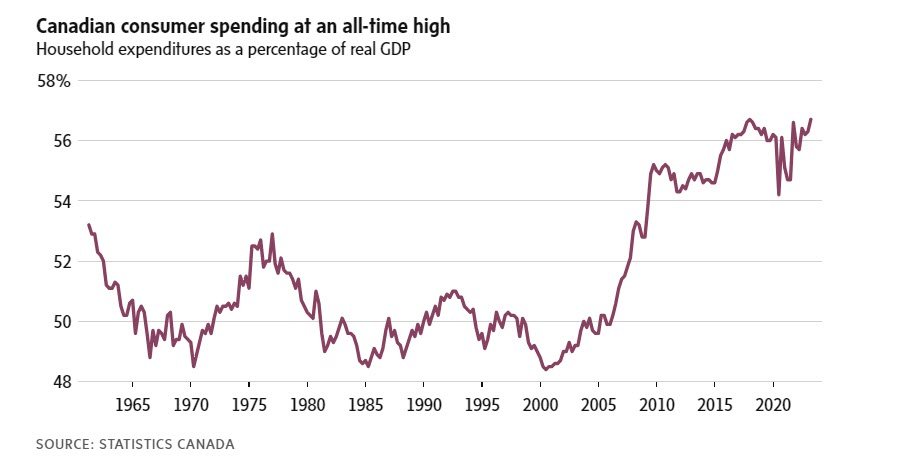

Consumers defy recession forecasts and spend, spend, spend!

Can we shop our way out of a recession? Consumers in Canada are giving it their best shot.

The strong first-quarter growth in GDP that caught economists off guard was powered by two sectors, exports and consumer spending, with the latter rising 5.7 percent on an annualized basis.

That growth was twice as fast as economists expected, and it pushed consumer spending to its highest share of GDP since records began in 1961.

South of the border, resilient consumers have been credited for helping stave off recession. But Canadian shoppers are outspending even their counterparts in the United States, where consumer spending rose 3.8 percent.

None of this is good news for the Bank of Canada as it tries to cool inflation by discouraging people from buying stuff. Instead, Canadians defied rate hikes and recession warnings to fork out for goods such as vehicles and services, including restaurants and hotels, at a frenzied pace.

The boom in services spending will have been particularly troubling to the bank. Governor Tiff Macklem warned in early May “the biggest upside risk to our inflation forecast is that services price inflation could be more persistent than we expect.”

This is why some economists believe the bank isn’t done tightening. “This is just the latest data point reinforcing the strength of the Canadian economy, particularly the consumer,” wrote Randall Bartlett, an economist with Desjardins. The shopping spree “substantially increases the odds of another rate hike.”

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third-party businesses, organizations and individuals featured in this newsletter. For more information, please visit https://www.ig.ca/en/legal.

May 20, 2023

Things to Consider When Deciding to Work with a Financial Advisor

When it comes to managing your finances, seeking professional guidance can be a wise decision. A financial advisor can provide valuable expertise, personalized strategies, and help you navigate the complexities of investment planning. However, choosing the right financial advisor is crucial. In this blog post, we will discuss the key factors to consider when deciding to work with a financial advisor.

1. Credentials and Qualifications:

Before engaging with a financial advisor, it's essential to verify their credentials and qualifications. Look for professionals who hold relevant certifications such as Certified Financial Planner (CFP), Chartered Financial Analyst (CFA), or Personal Financial Specialist (PFS). These designations demonstrate that the advisor has met stringent standards of education, experience, and ethical conduct.

2. Expertise and Specialization:

Consider the specific areas of expertise and specialization that a financial advisor offers. Some advisors focus on retirement planning, while others excel in tax planning, estate planning, or investment management. Assess your needs and find an advisor whose expertise aligns with your financial goals.

3. Fiduciary Duty:

Seek a financial advisor who operates under a fiduciary duty, which means they are legally obligated to act in your best interest. This ensures that the advice and recommendations provided by the advisor are unbiased and solely aimed at achieving your financial objectives.

4. Fee Structure:

Understand the financial advisor's fee structure before committing to their services. Financial advisors generally charge fees in one of three ways: a percentage of assets under management (AUM), an hourly rate, or a fixed fee. Evaluate these structures and choose the one that aligns with your financial situation and preferences.

5. Communication and Accessibility:

Clear and open communication is crucial when working with a financial advisor. Ensure that the advisor is accessible and responsive to your queries and concerns. They should take the time to understand your financial goals, explain complex concepts in simple terms, and keep you informed about the progress of your financial plan.

6. Client Reviews and References:

Take the time to research client reviews and testimonials about the financial advisor you are considering. This can provide insights into their reputation, quality of service, and client satisfaction. Additionally, ask the advisor for references from existing clients who can share their experiences working with them.

7. Compatibility and Trust:

Building a trusting relationship with your financial advisor is vital for a successful long-term partnership. Consider your compatibility with the advisor in terms of communication style, values, and overall rapport. A trustworthy advisor will prioritize your financial well-being and provide guidance based on your unique circumstances and goals.

8. Services Offered:

Evaluate the range of services provided by the financial advisor. Beyond investment management, some advisors offer comprehensive financial planning, tax planning, estate planning, and insurance advice. Assess your needs and choose an advisor who can provide a holistic approach to managing your finances. Working with a financial advisor can provide invaluable guidance and peace of mind as you navigate your financial journey. By considering factors such as credentials, expertise, fiduciary duty, communication, and client reviews, you can make an informed decision when selecting the right financial advisor for your needs. Remember, your financial well-being is at stake, so take the time to choose an advisor who will prioritize your goals and work with you to achieve long-term financial success.

Let’s meet! I’d love to hear about your financial goals and align these with the expertise that my team and I have to offer!

To book a meeting click this link and select ‘Meet with Sunshine’!

IG Wealth Management invites you to a Webinar: Finances and Dementia – Advice for the Journey

Today, there are more than 600,000 people living with dementia in Canada. By 2030, we can expect this number to be close to 1 million. Apart from the emotional and mental health impact, costs for people with dementia are 5.5 times greater than for individuals who have not been diagnosed with the condition.

Thursday, April 20, 2023 | 11 a.m. MT IG Wealth Management is a proud partner of the Alzheimer Society and as part of the Empower Your Tomorrow community program, we are committed to increasing the financial confidence of all Canadians. The seniors, parents, and grandparents of our communities often face unique financial challenges that come with age. For those facing a journey with dementia, the need for advice has never been greater. According to Christine Van Cauwenberghe, Head of Financial Planning at IG Wealth Management and author of Wealth Planning Strategies for Canadians, “I’ve been involved in many files where clients are starting to struggle with making financial decisions and it can be difficult for both the client and their family to navigate. Even a little planning in advance can help to reduce the stress.”

Gain valuable insight for the journey

Christine from IG will be co-presenting with Dr. Sarah Main, Research Scientist of The Alzheimer Society of Canada. Together, they will provide

Tips and tools for wealth planning for aging individuals

Advice for caregivers and people living with dementia

Tax considerations and resources available for Canadians

Webinar registrants will all have access to the playback of the event and a resource toolkit that includes a financial confidence checklist for people living with dementia and caregivers, a Power of Attorney guide, and information and resources from the Alzheimer Society.

With over 30 years of business development, critical thinking, and wealth management experience, Vas Pachapurkar brings an innate ability to communicate and connect ideas, tactics, strategies, and philosophies through his experience as a Consultant, Field Director, MFDA Panelist, and member of the National Distribution Leadership team. Vas is a proud graduate of Wilfred Laurier University and holds his RRC and CFP designations. Prior to IG Wealth Management, Vas worked with PricewaterhouseCoopers and Dresdner Bank AG.

Within his community, Vas has worked with the Make-a-Wish Foundation, the Herb Carnegie Foundation and Tour for Kids in partnership with Coast to Coast Against Cancer. Vas is also a driving force behind the IG Wealth Management Walk for Memories in support of the Alzheimer Society of Toronto. Vas and his family reside in Toronto, Ontario.

Featured speakers

Christine Van Cauwenberghe is the Head of the Financial Planning Division of IG Wealth Management. Christine obtained both her Commerce and Law degree from the University of Manitoba prior to being called to the Bar in both Manitoba (1995) and Ontario (2004). Christine spent several years practicing tax law with a large law firm in Winnipeg prior to joining IG Wealth Management in 2001.

Christine is a member of the Canadian Tax Foundation, has her Certified Financial Planner designation, is a Registered Retirement Consultant and is a Trust & Estate Practitioner, as certified by the Society of Trust and Estate Practitioners (“STEP”). She has previously served on the board of STEP Canada and is a recipient of a STEP Founder’s Award.

Christine is also the author of Wealth Planning Strategies for Canadians, which is published annually by Thomson Carswell and is currently in its 15th edition. She has published several industry papers, including with the Canadian Tax Foundation, the Canadian Association of Life Underwriters, the Law Society of Manitoba and the Estates, Trusts and Pension Journal. Christine has given lectures to numerous professional groups and is a regular media spokesperson for IG Wealth Management. Christine lives in Winnipeg with her husband and son.

Dr. Sarah Main is a Research Scientist for the Alzheimer Society of Canada (ASC), a leading not-for-profit health organization working nationwide to improve the quality of life and well-being of persons living with dementia and care partners.

Sarah has been on this career path for over 10 years, motivated by her family’s own personal experiences with dementia. Throughout this time, Sarah has led many dementia-focused initiatives and works with a range of collaborators, including persons living with dementia, care partners, and healthcare professionals to see these projects through. Sarah has been involved in creating regional dementia strategies, improving community-based supports, creating educational materials for healthcare professionals, and developing evaluation frameworks to support quality improvement efforts for numerous healthcare organizations, among other efforts. Sarah is committed to working alongside dementia advocates to illuminate and transform healthcare system inequities.

Sarah currently oversees the National Dementia Guidelines Program, which is a new strategic initiative launched by ASC to create standardized best practices that will improve experiences across the continuum of care for all impacted groups, including persons living with dementia, care partners, and healthcare professionals.

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third-party businesses, organizations, and individuals featured in this newsletter. For more information, please visit www.ig.ca/en/legal/disclosures.

Feb 28, 2023

How young Canadians are taking care of their mental well-being on a budget

It’s no secret that financial stress can take a toll on your mental health — especially at a time when Canada’s inflation rate remains high, layoffs are making headlines and there is talk of a looming recession.

Nearly one in four Canadians rank money as their top source of stress, nearly twice as much as personal health, work and relationships, FP Canada’s 2022 Financial Stress Index survey found.

One in three Canadians said financial stress has caused them anxiety, depression and other mental health challenges, according to the survey of 2,001 Canadians conducted by Leger.

Young Canadians are especially affected, the survey revealed, with 45 per cent of Canadians between the ages of 18 and 34 saying financial stress has hurt their mental health, compared with 31 per cent of Canadians aged 35 and up sharing that opinion.

Worrying about money can affect many facets of a person’s life, spanning their sleep quality, relationships and ability to work, said Stacy Yanchuk Oleksy, CEO of Credit Counselling Canada and a professional coach and a certified personal finance educator.

It can also exacerbate a person’s pre-existing mental health challenges, said Yanchuk Oleksy.

“Money and stress go hand-in-hand,” she said.

But despite their budgets growing more and more tight, some Canadians have found free and cheap ways to take care of their mental well-being — and they say it’s helped them to better cope with their financial stress.

About a year ago, Amy Dyck said she went through a rough patch and was experiencing a lot of mental distress. Through word-of-mouth, she was able to find help despite her financial constraints and started accessing virtual group therapy funded by Alberta Health Services.

“It’s free, thankfully, because I don’t think I could afford a one-on-one therapist,” she said.

Dyck said group therapy has helped her regulate her emotions and learn by hearing other people’s stories. It’s a resource that’s been especially helpful at a time when Dyck has been overwhelmed by the rising costs of living, she added.

“I don’t dwell on it or anything,” Dyck said of her finances.

If finances are weighing heavily on your mind and are starting to take a toll on your mental health, remember to breathe and realize that you’re not alone, said Yanchuk Oleksy of the Credit Counselling Society.

“Many, many Canadians struggle with this because it’s not something we’re taught. We don’t typically talk about it around the dinner table or in the classroom, but we’re expected at 18 to magically know how to manage our finances — and that’s kind of silly,” she said.

Oleksy suggests reaching out for support, whether it be a non-profit credit counsellor who can help you sort out your personal finances at little or no cost, or a mental health counsellor with whom you can discuss your mental health challenges.

Dyck said she recommends people speak to their doctor about the free and affordable mental health services that may be available to them.

Some therapists in Canada also offer sliding scales, meaning a cheaper rate for their services based on a client’s income.

K Kealey, a 27-year-old living in Calgary, said they were able to find a therapist with a sliding scale through Skipping Stone, a non-profit organization that connects trans and gender diverse individuals with low-barrier access to mental health services.

Kealey said they were previously accessing free therapy through Alberta Health Services, but they made the switch to their new therapist — who currently charges $80/hour — because they wanted to speak to someone who had experience working with trans and gender diverse people who could listen to them without judgement and help them navigate their transition.

“I find therapy pretty essential for figuring out things in my life and handling stress of work, money, relationships, all the things that you have to deal with,” said Kealey. “I don’t think I could’ve transitioned without that support, without probably burdening someone in my life.”

The Affordable Therapy Network is another resource that connects people to cheaper therapy options across Canada. This includes in-person therapy available in major cities and virtual therapy available throughout the country.

Katie McCowan, director and founder of the Affordable Therapy Network, said all of the roughly 450 therapists listed in the network’s online directory offer a limited amount of either low-cost rates — at $65 or less — or sliding scale rates, which are supplemented by others paying the full cost of therapy.

“People really need support. And (some people) really can’t afford (it) ... standard therapy’s about $150, oftentimes more, for an hour,” she said.

McCowan said she’s glad to see that access to therapy has improved in Canada over the years, but said she hopes to see more subsidized options in the future.

People should always reach out for help if they’re struggling financially, mentally, or both, Oleksy stressed.

“When you start to feel like you’re in control of your money, and you have a plan, it can kind of ease things up mental health wise,” she said.

“And vice versa, when you have a plan and a support system to deal with your mental health, it can give you a bit more breathing room to deal with your finances as well.”

To get the advice you need as a young person during these ever-changing times, schedule a meeting with an advisor from our team!

Jan 02, 2023

5 Things to Do Now to Propel Your Business in 2023

5 Things to Do Now to Propel Your Business in 2023

With the right playbook, entrepreneurs can survive and thrive in whatever economic scenario. Here are five things you can do to propel your business ahead now and through the difficulties of business cycles for years to come.

1. Learn the lessons of more challenging times

A rocky economy presents a unique opportunity to make tough decisions about the business plan. Everything is open to reexamination. How has the market changed? Are your customers facing challenges that create new opportunities for your solutions? How do new conditions change your assumptions, and what actions do you need to take in response?

Critically evaluate your product roadmap. Is this the time to pivot or become more aggressive with your current plans? Prioritize the highest margin features that are achievable in the next twelve months. Push out projects that don't make that list, and re-assign resources accordingly. Re-assess pricing. Even as inflation tiptoes back from the highest levels in forty years, raw material and transportation costs remain way up. What will impact your customers if you adjust the pricing or add surcharges to offset these costs, at least temporarily?

It's been a rough year for hiring. Many companies took the talent they could get. If there are employees or gig workers who would fare better in a different job, now is the time to let them go. Make tough-minded corrections that will pay off overall — corrections that might be avoidable in less challenging times.

2. Tighten your grip on cash

Venture capitalists are pulling back. In the third quarter, Crunchbase reported that funding for startups in U.S. and Canada fell 50% year-over-year. Valuations are down across the board. If you are fortunate enough to be a later-stage startup that benefited from VC largess in 2021, make your last raise last longer than intended.

Keep your dry powder dry, and put off going for another round until the markets even out. Reemphasize the basics for early-stage companies with less market validation and greater distance between now and a potential exit. Delay all capital expenditures. Leverage the hybrid work model if possible, to reduce rent and other office expenses. Continue with Zoom or Google Meet. Now is not the time to rack up travel costs. Re-negotiate fees and terms with service providers. Seek credit terms with key suppliers, in a word, bootstrap.

3. Talk to customers, in person. Now!

How have the business needs of your customers — whether paying or beta — changed over the last 18 months? Are there benefits to your solution that have more recognized value now? Nearly every business, for example, from corporates to startups, has been forced to re-learn the lessons of supply chain management. Startups that can help their customers make better business decisions based on artificial intelligence (AI), reduce costs by improving inventory management, or protect against out-of-stock scenarios by identifying and building relationships with new, more local sources of supply will have an edge.

4. Non-dilutive capital

According to PitchBook, venture capitalists are showing greater interest in portfolio companies "whose satellite, robotics and software tools can do double duty " in military and commercial markets. International conflicts are one reason, of course.

Another is that the defense and military security industries are generally viewed as recession-proof. Our firm routinely encourages portfolio companies to consider non-dilutive funding from the Small Business Administration — grants to support cutting-edge technologies range from $150,000 to more than $1 million.

Navigating the application process isn't for the faint of heart. A startup must be realistic about the work involved, but in many states, there are resources to help. Besides the funding, severe responses to agency requests for proposals are reviewed and evaluated by technologists. At a minimum, this can be terrific feedback and a great source of industry contacts.

5. Blue-chip cultures attract blue-chip talent

Company culture can be an asset or a liability. An inclusive, rich culture helps key hires say yes. Finding stakeholders that believe what you believe and are aligned with your team's values significantly improves the odds that they will stick with you in good times or bad.

After months of "great resignation" fever, the over-heated demand for talent may be cooling off. Maybe offers aren't as fast or grand as they were a year ago. Maybe Twitter won't be the only advanced technology business to let people go. Regardless, the search for great talent isn't a faucet that a young company turns off and on. A startup might modulate the timing or the number of hires but stand at the ready to recruit and filter for culture fit.

With the right mindset and intentional approach, an entrepreneur can make 2023 a year to strive and thrive. As Yogi Berra, my favorite baseball player of all time, said, "Swing at the strikes." In business, like baseball, the right swing can turn even the most challenging pitch into a hit.

Discover how to put these practices into action for your business and

book a meeting with Sunshine and her team!

Dec 12, 2022

Year end strategies to enhance your charitable giving

As we move toward the end of the year, we approach the season of giving. Many Canadians increase their charitable giving during this period. However, not everyone is maximizing their giving in the most tax-efficient way. Whether it’s a continuation of donations made throughout the year, or an initial donation, there are several strategies to consider when donating prior to the end of the year.

Maximize the value of donation tax credits

The first $200 of donations you claim on your tax return receive a lower donation tax credit rate than donations claimed above $200. To limit donations subject to the lower $200 credit rate, consider bringing forward donations planned early in the new year and make them prior to December 31st in order to combine them onto this year’s tax return. You can also maximize the amount above $200 by combining into a single tax return donations made by you and your spouse, and carryforward unclaimed donations made in any of the prior five years.

The federal donation tax credit is enhanced if your income is in the top tax bracket. Rules vary by province, but there may also be an increase to the provincial donation tax credit based on your income. If this is a high-income year, consider donating prior to the end of the year to take advantage of the potentially higher donation tax credit available to you.

Review your investment portfolio and donation opportunities

An additional tax incentive is available where publicly traded securities, such as stocks and mutual funds, are donated “in-kind” to charity. When the security is donated “in-kind”; any accrued capital gain is realized, however, the taxable portion of the capital gain is reduced from 50% to zero. Consider donating securities with large accrued capital gains, as opposed to cash, to enhance tax efficiency. You benefit from both the donation tax credit for the value of the security donated and eliminate the capital gains tax.

You may hold securities that are in a loss position, and you may wish to realize these capital losses for tax planning purposes to offset any capital gains you may have realized in the year. Donating the security to charity will realize the capital loss and generate a donation tax receipt, providing multiple benefits for your year-end tax planning.

If you have employee stock options for publicly traded securities; special tax provisions can exempt the taxable benefit resulting from the exercise of the option if the shares are subsequently donated to charity. After exercising the options; the shares, or the cash proceeds, must be donated within specified time limits to qualify for additional tax incentives. Planning, in collaboration with your IG Consultant, should be completed well in advance of the exercise of the options and any donation. The custodian of the options should be contacted to help coordinate the donation to your chosen charity. The applicable tax provisions are complex, and there may be limitations. Obtain tax advice specific to your circumstances. If you wish to donate securities before the end of the year, don’t wait until the last minute as additional time may be required for the financial institution and charity to process the request.

Time TFSA withdrawals used to make donations before year-end to restore contribution room quickly

You may wish to withdraw funds from your TFSA to fund a charitable donation. A TFSA withdrawal is tax-free, however, contribution room will not be restored until January 1st of the following year from the withdrawal. Plan to make your TFSA withdrawal prior to the end of the year so that your TFSA contribution room is restored on January 1st of the following year. This gives you the extra flexibility to re-contribute amounts to your TFSA in the new year and utilize donation tax credits on this year’s tax return.

Keep track of donation receipts

Often donation receipts are received immediately rather than being distributed in the new year. These receipts may be issued physically or by email. As you receive your donation receipts throughout the year keep a record and file them. This will make it easier to locate these receipts when it’s time to file your tax return.

Establish a donor-advised fund

A donor-advised fund can be beneficial in any charitable giving strategy. You can setup an account, name it as you so wish, and receive the tax benefits from donations. Assets can grow on a tax-exempt basis; and you retain control by recommending investments, grant amounts, and recipient charities. You may wish to give to charity before year-end but have not yet decided which causes to support, and a donor-advised fund may provide an appealing solution.

Consider setting up a donor-advised fund with the IG Wealth Management Charitable Giving Program - a partnership between IG Wealth Management and the Strategic Charitable Giving Foundation. The program can help you create a lasting legacy by facilitating grants over an extended period or in perpetuity to the charities you choose. If desired, your family members can assume responsibility for recommendations on the account after your death or incapacity, establishing a multi-generational tradition of philanthropy. Discuss with your IG consultant how you and your family may benefit from creating a donor-advised fund.

As you can see, there are many considerations when deciding to give to charity. It is important to seek advice to help navigate these issues and maximize benefits both for you and the causes you care about. For more information on charitable giving and how it fits into your plan, speak to your IG Consultant.

Written and published by IG Wealth Management as a general source of information only, believed to be accurate as of the date of publishing. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal, or investment advice. Seek advice on up-to-date withholding rules and rates and on your specific circumstances from an IG Wealth Management Consultant. Trademarks, including IG Wealth Management and IG Private Wealth Management, are owned by IGM Financial Inc. and licensed to its subsidiary corporations.

Nov 16, 2022

Hockey Hall of Famer and IG Wealth Legend!

Herb Carnegie in 1953

IG Wealth Management is delighted to share that hockey pioneer and Order of Canada recipient Herb Carnegie has finally been inducted into the Hockey Hall of Fame.

Herb was arguably the best Black player to have never played in the NHL as he, unfortunately, faced numerous challenges and barriers due to the racism of the day.

Despite the racism he faced, Herb played hockey in various leagues from the 1930s into the 1950s, often standing out as the best player on the ice. When he retired from hockey, he took over the financial industry.

Herb was one of the true legends of IG Wealth Management. He spent 32 years with IG (then Investors Group), serving clients with excellence as he carried his passion from the ice to his community.

In 1987, Herb founded his hockey school, Future Aces, and the Future Aces Foundation to “inspire and assist youth and adults to become the best they can be as responsible, respectful, peaceful, confident and caring citizens.” Herb’s values have been engraved in the teachings at Future Aces, including kindness, treating people well, and appreciating who you are.

To honour Herb, IG created the Herbert H. Carnegie Community Service Award in 2003 to recognize advisors who demonstrate extraordinary dedication and service to their communities.

Congratulations to the entire Carnegie family on this achievement – we couldn’t be prouder!

Nov 12, 2022

Not All Advisors are Created Equal!

Not All Advisors are Created Equal

In a recent study (Oct 27, 2022)on Canadians and personal financial planning conducted by IG Wealth Management,Christine Van Cauwenberghe, Head of Financial Planning, underlined the importance of appreciating that, although many financial institutions may have staff who are capable of completing transactions, not all may be able to provide the full scope of financial planning services required, including the ability to provide comprehensive advice.

“When you’re choosing a financial advisor, verify their credentials to ensure that they have expertise in financial planning. You should also make sure that they take the time to get to know your personal situation and identify your individual objectives before immediately recommending specific products. Some advisors are only capable of providing investment advice and will start suggesting specific investment solutions before they’ve asked you many questions – that’s a flashing red light that they are more concerned about selling a product than creating a plan that meets your needs”.

In fact, the study found:

One-fifth (21 percent) of Canadians go to retail bank-based representatives for complete financial advice.

Almost half (46 percent) of Canadians expect advice on their financial health from where they do their banking, but only 29 percent say they actually receive this.

“Canadians deserve more when it comes to financial advice,” stated Ms. Van Cauwenberghe. “It’s important to understand that not all bank-based representatives are certified financial planners. While you may feel comfortable going to your financial institution for guidance on loans or investing, you may be missing out on crucial advice about all the other aspects that should make up a financial plan.”

You deserve more! Contact me and my team and get the advice you need to acquire true richness in life!

Click below and go to ‘Meet with Sunshine’ to book an in-person or online meeting!

Nov 08, 2022

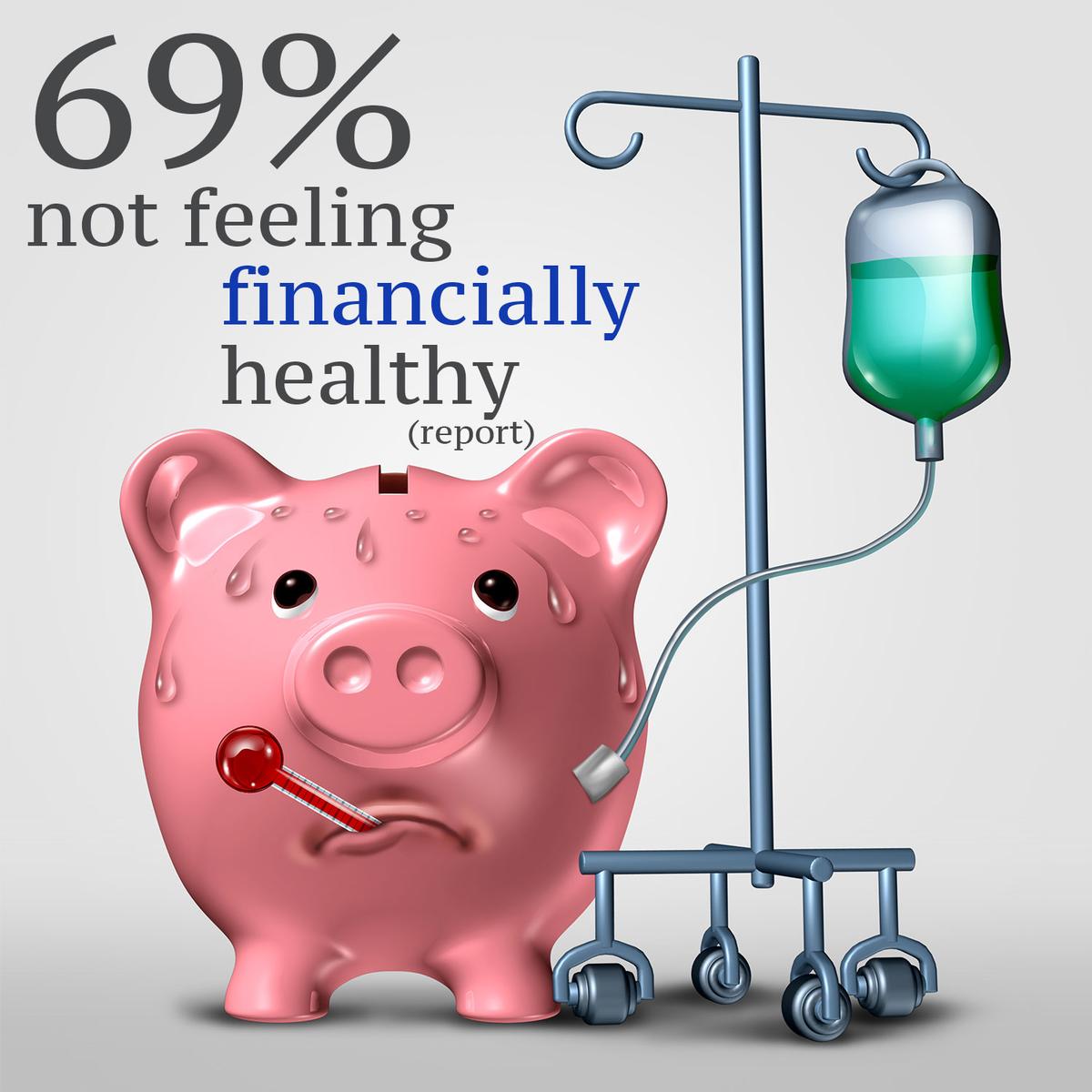

Canadians Feeling Uncertain About Personal Finances

Over two-thirds (69 percent) of Canadians report not feeling “financially healthy” given current economic conditions.

Almost half (46 percent) expect advice from their banking institution, but only 29 percent say they actually deliver on this.

WINNIPEG, MB – October 27, 2022 – In advance of Financial Literacy Month,IG Wealth Management (IG) today released a study on Canadians and personal financial planning. According to the study, Canadians are feeling uncertain when it comes to their personal finances. However, those who use a financial advisor are much more likely to feel secure and “financially healthy” as they navigate current market conditions.

The study, conducted in partnership with Pollara Strategic Insights, found:

Sixty-nine percent of Canadians stated that they are not feeling financially healthy as a result of recent economic conditions.

Two-fifths (44 percent) say they are getting by financially but could be better off.

Similarly, 44 percent worry they are not handling their finances in the best way possible.

One-third (31 percent) of Canadians who do not work with a financial advisor are worried about their finances. However, this number drops to just 16 percent among those who do work with one.

“It’s understandable that so many Canadians are feeling insecure about their personal finances given everything they’re seeing out there, whether it be market volatility, inflation or rising interest rates,” said Christine Van Cauwenberghe, Head of Financial Planning, IG Wealth Management. “In many cases, people may feel overwhelmed and uncertain of how to navigate current market conditions. It’s not a surprise that those who take advantage of the advice provided by a qualified financial advisor are less likely to be concerned about their situation.”

Ms. Van Cauwenberghe noted that, in times like these, it is especially important for Canadians to work with a financial advisor who has the knowledge and expertise to review all aspects of their financial world and ensure they have a holistic financial plan so they can make better decisions and feel more confident.

Connect with a local advisor in St Albert! Click the link below to learn more about and connect with Sunshine Pawchuk, Division Director/CFP professional, and her team at IG Wealth Management in St Albert.

Jun 13, 2022

Buy now, pay later becoming a lifeline for young business owners

Taran and Bunny Ghatotra run Blume — a seven-figure, skincare and period products company.

The sisters initially began in 2016 with a subscription business for organic period care products, when Taran was 23 and Bunny was 21. They learned they had to get creative to get their dream funded, since accessing capital through bank loans and getting credit with suppliers was difficult in the early stages.

“Often [banks] need to see some kind of collateral or a certain amount of inventory or profitability. So obviously, as a brand new business, you don’t always have those things,” says Taran, who lives in Vancouver, B.C.

A recent Angus Reid Institute survey conducted in conjunction with Tabit — a buy now, pay later (BNPL) platform at point-of-sale for small businesses — found that over half of Canadian small business owners would consider an alternative financing option at checkout where payments are made in installments over time.

And younger owners (aged 18 to 34) were twice as likely, compared to older owners, to “definitely” consider this type of financing solution.

What are the benefits of BNPL platforms for businesses?

“The smaller the business, the higher the risk from a lot of banks’ perspectives,” says Corinne Pohlmann, senior vice-president, national affairs and partnerships for the Canadian Federation of Independent Business (CFIB).

“It also depends on, are you at the beginning of your business stage or your startup? … And what is the reason for the capital needs?”

It can be difficult for a young business to get approved for a bank loan, but there are other options when it comes to funding and dealing with expenses. BNPL can essentially work as a loan, but young business owners are more likely to be approved for it.

BNPL has already gained popularity in the consumer space, especially among younger shoppers — and it’s now making its foray into the business-to-business world in Canada.

“What you need is a way to automatically come up with a credit decision, right at checkout with no delay, and that’s not easy, especially in business transactions,” says David Gens, president and CEO of Merchant Growth and Tabit.

Tabit — which launched in February this year — functions as a third-party platform to allow businesses to pay their suppliers in weekly installments. It’s a first for Canada, although BNPL services for the business-to-business space are available in other countries, like Resolve, Billie, Apruve, and Slope.

“We’re providing more credit to more businesses to make more purchases, but we’re also streamlining things for that supplier,” says Gens.

Banks typically secure loans against assets like real estate or inventory, with these assets acting as collateral. In contrast, BNPL platforms may use algorithms, credit checks, or other scoring mechanisms in order to approve a business.

With this system, Tabit approves more small businesses for unsecured loans, where no collateral is necessary. Unlike bank loans or credit cards, Tabit also doesn’t currently report to the credit bureaus, which means that if you don’t make your payments on time, it won’t affect your business credit score.

The length of the payment time may vary. For Tabit, it ranges from one to 12 months, while Resolve offers 30-, 60- or 90-day terms.

How does BNPL work for small businesses?

Taran says Blume doesn’t use a third-party platform but directly negotiates with its suppliers to pay in installments.

“You want to make sure that you can afford the payments when the time comes, and that you’re really managing your cash flow adequately, but I think it can be really meaningful for small brands to be able to use that money for marketing and growth until you get paid.”

However, it often takes time for businesses to build a good relationship and earn credit with suppliers.

While BNPL platforms take on the responsibility of approving small business buyers and paying their suppliers, be mindful that there may be extra fees or penalties involved.

Resolve and Billie, for example, don’t charge fixed fees or interest rates to buyers. Instead, the suppliers are charged fees. If payments are not made on time, Resolve or Billie may be able to offer extended payment terms. However, in a worst-case scenario, the companies may utilize collection agencies to secure repayment.

Tabit features zero percent interest for up to 90 days. Merchants pay a fixed fee to offer the zero percent option to buyers, but in other cases, the buyer will need to pay a fee based on things like their risk profile, sales or industry.

Gens explains that Tabit will work with buyers if they’re struggling to meet their payment terms, but may need to use legal means if the buyers are unresponsive or refuse to cooperate.

BNPL for businesses could be potentially beneficial for cash flow and creating competition, says Pohlmann, but adds that there may be downsides as well.

“Having a few more options that can maybe help [owners] deal with expenses that they need to actually incur in order to get their business back on its feet, there may be some potential here. But there also can be some drawbacks if you end up paying more overall [on interest or fees].”

What other options do small businesses have when it comes to financing?

Pohlmann says some business owners may turn to family members or friends for financial help, use credit cards or dip into their personal savings.

“In the early days, we definitely used our own credit card debt and student loans, and bootstrapped them,” says Taran.

Taran adds that she and her sister acquired their first loan from Futurpreneur — a Canadian non-profit that supports young entrepreneurs — and later raised funding from angel investors and venture capitalists.

However, relying on credit cards and personal savings accounts can fuel debt. The CFIB reported in March that two-thirds of businesses have taken on debt, at an average of $158,000 per business.

Taran suggests looking into grants, although Pohlmann says these aren’t always accessible to everyone.

“There aren’t a lot of them … they’re often very specific and targeted, and can come with a lot of paperwork.”

Pohlmann advises small business owners to explore different options.

“Don’t just go to the traditional banking route, see what works best for your business. Figure out the amounts that you need … and how much you can afford as a business to take on … You may have family or friends that are also willing to help you out.”

May 20, 2022

Leave your children the vacation property, not a tax bill

A vacation property—whether it’s a cottage in Muskoka or a chalet at Tremblant—is a valuable asset, not just in terms of the real estate, but also as aplace that holds years of family memories. For many Canadians, passing the property to the next generation is a priority, but there are significant tax and non-tax-related considerations associated with keeping that cabin or condo in the family.

Do your children want the property?

The first thing to consider is whether your children or grandchildren are interested in owning the property. Although they may enjoy spending time there with you, there’s no guarantee that they will be interested in maintaining or using the property after you’re gone; particularly if they live in another province. If you have more than one child, you will also need to determine if they are interested in sharing ownership and responsibility for the property with their siblings.

Once you’ve confirmed that your children are interested in owning the property, it’s important to think about the tax liability that inheritance will trigger for them and make plans to help mitigate the impact.

Tax implications

When a vacation property passes to anyone besides your spouse or common-law partner at the time of your death, it will trigger a tax liability for your estate based the appreciation in the value of the property. That appreciation is calculated using the fair market value of the property at the time of transfer, less the purchase price and the cost of any improvements made to the property during your period of ownership. As your vacation property may have increased considerably in value over the years, the concern is that the tax liability could be so large that your beneficiaries may have to sell assets—possibly the vacation property itself—to meet the tax obligation. Making provisions for the transfer of your vacation property as part of your estate plan is, therefore, essential.

Strategies for mitigating the tax impact

Using the principal residence exemption

One possible way to reduce the tax liability is to designate the property as your principal residence to exempt some or all of the capital gains on its disposition from taxation. Keep in mind that your family can only have one principal residence in a given year, but you don’t have to designate which property that is until you sell it or are deemed to have disposed of it (as you would in the year of your death). Your executor or liquidator should consult with your tax and financial advisors to determine how to use the principal residence exemption to best advantage.

Preserve the adjusted cost base

The taxable capital gain on your vacation property can be reduced by increasing the adjusted cost base (ACB) of the property. The ACB is increased by adding the costs of property improvements made over the years to the initial purchase price. So, be sure to keep records and receipts for materials and professional fees paid for renovations and upgrades.

Using insurance

If your estate doesn’t have sufficient liquid assets to cover the capital gains tax that will be triggered by the transfer of your vacation property, consider using life insurance to cover the liability. Your children may even be willing to pay the premiums on a life policy if it means being able to keep the property without having to cover a large tax bill down the road.

Gifting during your lifetime

As is the case with a transfer of a vacation property upon death, gifting a property during your lifetime will be deemed to have occurred at fair market value (unless you transfer the property to your spouse). This means you will be liable for tax on the capital gain calculated as the difference between what you paid for your vacation property and what it’s worth now. If you choose to sell a property to your children during your lifetime for less than its fair market value, you will, regardless of the selling price, be deemed to have received fair market value and will be responsible for the tax on difference.

Although capital gains taxes on the disposition of a vacation property cannot be avoided by gifting it during your lifetime, one potential advantage of this strategy is limiting the amount of tax payable by gifting the property at its current market value, rather than its potentially higher value at the time of your death.

Co-ownership considerations

If one or two of your children want the vacation property, but others do not, the issue may become how to equalize the estate, and you may want to consider using insurance to help fill the gap.

If several children want the property, then you should also consider having a co-ownership agreement between them created before the property is transferred (and possibly as a condition of inheritance). Such an agreement outlines how the property will be used, who is responsible for its upkeep, and how the property will be passed on in the future.

U.S. and foreign properties

There are different and significant tax implications pertaining to the succession of vacation properties outside of Canada. When considering purchasing or passing on such properties, it is important to speak with a cross-border tax advisor.

As you can see, it’s important to plan for how a vacation property will be passed on to the next generation long before it happens.

For more information, ask me for copies of our white papers, Vacation Property Succession Planning and Canadians Owning Vacation Properties in the U.S.

Written and published by IG Wealth Management as a general source of information only, believed to be accurate as of the date of publishing. Not intended as a solicitation to buy or sell specific investments, or to provide tax, legal or investment advice. Trademarks, including IG Wealth Management and IG Private Wealth Management are owned by IGM Financial Inc. and licensed to its subsidiary corporations. Insurance products and services distributed through I.G. Insurance Services Inc. (in Québec, a Financial Services Firm). Insurance license sponsored by The Canada Life Assurance Company (outside of Québec).

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third party businesses, organizations and individuals featured in this newsletter. For more information, please visit https://www.investorsgroup.com/en/legal/disclosures.

May 01, 2022

7 Factors That Affect Your Life Insurance Quote

Over a period of years, even a slightly lower life insurance premium can yield major savings. The following are some of the biggest factors that insurers consider when pricing out their policies. Some of these criteria are outside your control, while others are things you can remedy with simple lifestyle choices.

KEY TAKEAWAYS

Life insurance can be financial help for your loved ones once you're gone, but it's a big investment.

Many factors contribute to how high your premium payment is and whether you qualify for discounts.

Age is the most important factor in determining the cost, as a younger person will make payments for many years before cashing out; therefore the younger you are, the lower your payments tend to be.

Gender is also a crucial factor since women statistically live five years longer than men; as a result, insurance carriers typically offer women slightly lower premiums.

Smoking, health, lifestyle, family medical history, and your driving record are the other key determinants of how much you might expect to pay for life insurance.

Life insurance quotes are based on several factors, some of which may be beyond your control; when researching policies, consider the seven factors here and choose an insurer less likely to penalize those in your particular position.

1. Age

Not surprisingly, the number one factor behind life insurance premiums is the age of the policyholder. If you’re young, the chances are that you’ll be paying the insurer for years before they ever have to worry about writing your family a check. Consequently, you’re better off taking out a policy before it’s too late. But that doesn’t mean you need insurance right after college if you don’t have any financial dependents.

2. Gender

Next to age, gender is the biggest determinant of pricing. Insurance carriers use statistical models to approximate how long someone with a specific profile will be around. The fact is that women, on average, live nearly five years longer than men.1 And because they’re usually paying premiums for a longer period of time than males, they enjoy slightly lower rates. Sorry, guys.

3. Smoking

Smoking puts you at a higher risk for all sorts of health ailments. So if you like to light up, it’s a red flag for insurance companies. In fact, it’s not uncommon for smokers to pay more than twice as much as non-smokers for comparable coverage. The effect on your pocketbook is another great reason to try and kick the habit.

4. Health

The underwriting process for most carriers includes a medical exam in which the company records height and weight, blood pressure, cholesterol, and other key metrics. They may also require an electrocardiogram (ECG or EKG) to check your heart in some cases. It’s important to get any serious conditions like high cholesterol and diabetes managed before searching for coverage to ensure a competitive rate. Some companies do offer “no exam” policies, but you can expect to pay more.

5. Lifestyle

Is your favorite pastime racing cars or climbing treacherous mountains? If so, you’ll probably have to shell out substantially more for insurance. Any time you engage in high-risk activities, there’s an increased likelihood that you’ll meet an early end – a big concern for carriers. Some companies also charge more if you have a relatively dangerous profession, such as mining, fishing, or transportation.

6. Family Medical History

There’s not much you can do about your gene pool. However, a family history of stroke, cancer, or other serious medical conditions may predispose you to these ailments and lead to higher rates. Carriers are usually interested in any conditions your parents or siblings have experienced, particularly if they contributed to premature death. Some carriers put more emphasis on your family’s health than others, but it’s likely to have some impact on your premium.

7. Driving Record

It may come as a surprise, but many life insurance companies look at your driving record during the underwriting process. Whether or not they ask about violations on the application, they can access Department of Motor Vehicles records to find out if you’ve run afoul of the traffic laws. Keep in mind that the last three to five years carry the most weight, so if you’ve improved your driving habits, you may benefit from a more favorable price.

Article Source:

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

Apr 27, 2022

What to do if the CRA asks for more information...

You filed your taxes on time, and you’re expecting a refund. Instead, the Canada Revenue Agency (CRA) contacts you to clarify some details about your return. There’s no reason to panic. The CRA occasionally contacts people for more information and things can be cleared up quickly, if you’re prepared.

Why does the CRA reach out?

The CRA can contact individuals for any reason. In most cases, they may want further details about an item you’ve claimed on your return, including:

Medical expenses

Capital gains related to the disposition of real estate

Consistent losses from self-employment income

Vehicle expenses

Foreign tax credits

Significant changes from your filing history

The CRA is typically seeking documents that will verify your claims. For example, if you’ve claimed unusually high medical expenses, they may want you to provide detailed receipts.

Verify that it’s the CRA contacting you

In most cases, the CRA will contact you by sending you a formal letter when requesting additional information. They may also call you or send you a secure message directly to your CRA online account.

That said, fraudsters can contact you via phone posing to be a CRA agent. Here are a few things to consider before you provide any information:

A legitimate CRA agent will provide their name, number, and office location. With that information, you can contact the CRA directly to verify the person’s identity.

CRA agents will not use aggressive language or pressure you into making quick decisions.

The CRA does not ask for payments in cryptocurrency, prepaid credit cards, or gift cards.

The CRA will never ask you questions unrelated to your tax return, such as your credit card information.

CRA agents will never offer to apply for benefits on your behalf.

Respond to the CRA

Once you’ve verified the authenticity of the request, you can gather the required documents. The letter will typically describe exactly what you need to provide. You’ll also want to make note of the reference number (included in your letter), the date you need to respond by, and the office that’s handling this request.

Before you send your documents, make copies so that you can keep them for your own records.

Once you’re ready to submit your documents, you have the following options:

Login to your CRA online account and upload all of your documents.

Send the documents by standard mail. Be sure to include a cover letter that lists your reference number and any other relevant details.

Fax your documents. The fax number should have been provided in the request letter.

When uploading files online, you’ll get a confirmation number: Keep the number for your records. If there was a problem with any of the files or documents received, the CRA may request that you resubmit them.

Keep all your records on file

Since there’s no way of telling what information the CRA may ask for, you need to keep all your records, or at least have access to them for at least six years following the relevant tax year.

This six-year rule would apply to all your tax documents, not just expenses. In other words, hang onto all your income statements, receipts, and any other relevant documents. There’s always a possibility that the CRA asks to review or audit your taxes at a later time. Having all your documents in one place will ensure that you’re prepared.

What happens if you don’t respond

If you choose to ignore the request for additional information, or you forget to respond, the CRA may reassess your tax return. That could result in taxes owed, penalties, and interest payments. Plus, there’s a possibility that your tax return could be flagged for further review, such as an audit.

If you’ve filed your tax return honestly, there’s no reason to fear any requests from the CRA. All they’re looking for are details, especially if there’s been a major change to your income or expenses. Most of the time when you provide the supporting documents, you won’t hear from the CRA again until you get your notice of assessment.

Click the link to book a meeting to learn more about your taxes or other financial matters!

The Canada Emergency Response Benefit (CERB) has been a lifeline to millions of Canadians as they navigated the turbulence of the COVID-19 pandemic.

As we are all aware, many businesses were forced to close down or vastly reduce their operations in 2020 to comply with their regional or local public health orders to reduce the spread of this virus. This situation directly led to millions of Canadians losing their jobs or being furloughed until their employers were able to open up again.

CERB was introduced to provide financial support to both employed and self-employed Canadians whose income was directly affected by COVID-19. Eligible applicants for CERB could receive $2000 for every qualifying 4-week period ($500 per week) between March 15 and September 26, 2020.

This was a welcome program for many Canadians during this tumultuous time, providing income to 8.9 million individuals across the country when they could not work through no fault of their own.

With tax season on the horizon, now is an excellent time to take stock of how these benefits will affect your taxes if you haven’t already.

CERB is a taxable benefit, so it will count towards the individual’s income for the year when they file their 2020 tax return. However, unlike most people’s pay from their employers, the income tax for these benefits was not withheld when they were paid out, so this could make for a very unwelcome surprise at tax time.

Calculating the tax owing on the CERB benefits can get a little tricky because all of a person’s income from before and after they received these benefits also needs to be accounted for, in order to add up the individual’s total income for the year. Once a person has this figure, there are free online income tax calculators for 2020 that will help them work out how much federal and provincial tax they will owe, such as the one at Wealthsimple (https://www.wealthsimple.com/en-ca/tool/tax-calculator/). Once the person knows how much tax they will owe for the year, they can calculate how much tax is due for the CERB benefits. Divide the total tax figure by 52 to get a weekly figure. Then multiply the weekly figure by the total number of weeks that the CERB benefit was received for the year. This will give the amount of taxes that are owed on the CERB benefits.

If you received CERB benefits in 2020, it is a good idea to ensure that you have enough money set aside to cover the taxes that will be owing on these benefits. If you haven’t put anything aside to cover these taxes, start as soon as possible. If you don’t think that you will have enough set aside to pay these taxes, consider contacting the Canada Revenue Agency to arrange a payment plan (https://www.canada.ca/en/revenue-agency.html).

This tax situation can get overwhelming but being proactive now can prevent a nasty shock down the road.

Dean LaBerge, Local Journalism Initiative Reporter, Grizzly Gazette

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third-party businesses, organizations, and individuals featured in this newsletter. For more information, please visit https://www.investorsgroup.com/en/legal/disclosures.

Find out how you can improve your financial well-being score!

Jan 21, 2021

Trump’s Out; Biden’s In: What You Need To Know If You’re Invested In Stocks

Trump’s Out; Biden’s In: What You Need To Know If You’re Invested In Stocks

America is in turmoil and many are worried about a massive correction in stocks. While a correction is inevitable at some point, in the near-term, the odds are against it. In this article, we’ll discuss what really drives the stock market and how the recent turmoil is nothing more than extraneous noise for investors.

AFP via Getty Images

Emotional Investing: A Recipe for Disaster

We are emotional creatures (even those who are highly analytical), and as such, we all have feelings. Moreover, it is our thoughts that form our beliefs and our feelings (emotions) tend to dictate our actions. This is a subject that has been studied at length. Nonetheless, if we can control our emotions, we can minimize investment mistakes. Have you ever heard that we shouldn’t make important decisions when we are highly emotional? This pandemic, coupled with the plethora of mis- and disinformation on social media and some extreme news sites, has created a highly emotional citizenry. Thus, while it is disappointing, we shouldn’t be terribly surprised at the type of behavior we’ve witnessed. As repugnant as it may be, it has little to do with the directional trend of the stock market. Therefore, don’t let your emotions control your investment decisions.

Politics, Profits, and Stocks

A common investment mistake is connecting politics with stock market performance. Stock prices rise and fall based on corporate profits, period. Thus far, corporate profits have been good. Even though many things affect profits, the current political climate is not one of them. More on that in a moment.

Economy & Stocks

The stock market is not wholly connected to the economy. A study in the 1990s by Goldman Sachs demonstrated that only about 40% of stock performance can be attributed to the performance of the economy. Thus, it is a link worth considering. Approximately 70% of U.S. economic growth is derived from consumer spending. Therefore, when consumers spend, the economy thrives. Conversely, when consumers hold back, the economy tends to suffer. In 2020, consumer spending fell 1.55% for the year. However, from April 1, 2020 to the end of the year, consumer spending increased 20.27%, thanks in part to federal government stimulus. Although the economy ebbs and flows, we must be mindful of its long-term trend, which is almost always higher.

Politics, Social Unrest, & Stocks

I mentioned that politics and stock market trends are not connected. There is an exception to this, but we have not seen it in the U.S. in the modern era. In a third world country where markets are not as free, if a dictator decided to employ a chokehold on businesses, stock performance would surely suffer.

U.S. stock markets have survived numerous social and political events. For example, when President Kennedy was assassinated November 22, 1963, stocks fell 2.89%, then immediately rose, logging a 17.0% return for the year. Even during the mass rioting that swept America between 1963 and 1968, stocks held up well. When Martin Luther King Jr. was assassinated April 4, 1968, stocks lost 0.77% the following day, then rose, ending the year with a 4.27% return. Though social unrest is very disturbing, it has had little to do with stock market performance. This is vital to understand, especially with emotions running high.

Politics, Socialism, and Stocks

Some are concerned over the prospect of America’s trend toward socialism. I am also concerned. Does socialism cause stock performance to suffer? I propose that America is already steeped in socialism, beginning with FDR in the 1930s, and continuing with LBJ in the 1960s. Though I am not an advocate of socialism, one has only to look at Europe to understand that financial markets can exist and function well, even under socialism. I AM NOT suggesting there should be no concern, but as far as the financial markets are concerned, it is not an issue at this time. Again, it’s important to separate our emotions from our investing.

Why Politics Have Little Effect on Stock Performance: Who Really Runs America?

Princeton and Northwestern Universities conducted a study on the amount of political control/influence of ordinary citizens compared to corporate America. Looking at data from 1982 to 2002, here’s what they learned. If large corporations and wealthy individuals wanted a law implemented, there was a 60% chance it would pass. If the same group didn’t want a new law to be passed, there was a 100% chance it would fail. For ordinary citizens, the numbers were 30% and 30% respectively. Thus, it is corporations that most often influence policy, not ordinary citizens or even the government. Although government officials debate and vote on legislation, it is often at the behest of corporations. Think about that for a moment. Since corporations wield great power, they will tend to resist laws that would be detrimental to their business.

But there’s another important point to make here, which is connected to my statement that financial markets can do well, even under socialism. Corporations hate uncertainty. If the rules are clear and there’s a way to make a profit, they will find it. This is why corporations often donate money to both parties.

Why Stocks Could Continue to Trend Higher

If much of what we hear in the news is not that pertinent to financial market performance, what is relevant? Today, it is Covid-19 and the vaccine, stimulus, interest rates, and liquidity. First, if enough people are vaccinated before the current surge in cases gets too bad and before it mutates beyond the scope of the vaccine, we will be able to put this terrible episode behind us. Next, stimulus is a major factor. With democrats in control of Washington, the stimulus faucet will be unclogged and that will provide great support for the economy (which helps corporate profits and stock prices). Next, interest rates are low, providing cheap money for corporate borrowing, which can help companies grow. Finally, the Fed has expanded the money supply to assure plenty of liquidity for markets to function properly. Remember 2008? An enormous part of the problem was that liquidity dried up.

As investors, we must learn to dismiss the “noise” and focus on what’s relevant to financial markets. We must also learn to separate our feelings on social and political issues from our financial decisions. Yes, America may be in the throes of a tumultuous period, but this too shall pass. The pendulum may swing far left, then far right, but this has been a common occurrence throughout history. America will indeed survive this as well.

Despite recent events, as far as stock markets are concerned, much of it is noise and has little effect on how stocks perform.

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third party businesses, organizations and individuals featured in this newsletter. For more information, please visit https://www.investorsgroup.com/en/legal/disclosures.

Jan 08, 2021

Want It In 2021? Measure It.

Think back to the start of the new year one year ago, and the goals you had for yourself and your team. What were those goals? Were many of them (or any of them) achieved? Did too many get shelved amid the new rhythms of doing business virtually?

As we embark on a new year that’s starting out with a bumpy ride, what key initiatives do you consider to be your top priorities to take your team to the next level?

To answer that question, I recommend following these steps:

1.Collaboratively set the goals. Many times, I’ve seen leaders set goals and then roll them out to their co-workers. This authoritarian approach to goal-setting may result in compliance and maybe even some achievement, but rarely does it result in genuine enthusiasm, creativity, and discretionary effort.

On the other hand, collaborative goal setting can result in strong buy-in and excitement that propels the team to success. I encourage leaders to provide their co-workers with some high-level concepts or direction and then invite their team to share what they believe should be the priorities. Eric W. Bennett, chief investment officer and co-founder of Tolleson Wealth Management in Dallas, which is one of my clients, says, “I am very intentional about having an engaging brainstorming process with my team that results in our team goals, not my goals. When doing goal planning, we create an environment that encourages people to think differently, creatively, and candidly. I believe this results in more engagement and buy-in from the team, and better ideas than if I was just pushing my own goals on the team.”

2. Establish specific measurements of success. For each goal, answer questions such as:

• What quantitative measurements will be established to gauge success?

• Instead of just one measurement at the end, can milestones along the way be established?

• What dates apply to each measurement?

• Who is specifically responsible for each goal’s achievement?

• Do team members feel like they are in control of their success?

3.Constantly communicate progress. Map out a communication plan with your team. Come to agreement about who is responsible for sharing progress for each goal, plus when and how that person will share updates about progress.

4.Celebrate achievements along the way and at completion. In the competitive financial services industry, many leaders do not make celebrating achievements a priority. When a goal is achieved, many times they’re already moving on to the next topic without genuinely celebrating and acknowledging success. Financial rewards are great but they do not take the place of emotionally engaging the team by celebrating success together.

In terms of specific goals, I’ve observed teams frequently focus on initiatives related to technology upgrades, sales, activity-based benchmarks such as client calls, asset retention, and marketing initiatives. In addition to these, I’m encouraging my clients to also consider foundational goals, such as:

• Strengthening specific behaviors that may have weakened in a remote environment, such as candor, appreciation, accountability, and actionable feedback.

• Employee development beyond required compliance training or new technology mastery. Team building, leadership development, and other training opportunities let staffers know you continue to invest in each of them

• Gauging team culture—where it is now, how it changed over a challenging year, and where you want it to be this time next year.

• Addressing talent gaps through training incumbents or targeted hiring.

• Creating or updating your team’s succession plan to manage expectations and ensure thoughtful transitions.

Whatever goals you choose, the likelihood of successful achievement is significantly higher when you establish specific measurements and (this is also essential) share those measurements with others who will hold you accountable, such as coaches, advisory boards, or colleagues outside of your team. Taking steps to control what you can by thoughtfully setting targets can unite your team and be key to this new year being a breakthrough year.

Fran Skinner, CFA, CPA, is a partner at AUM Partners, a Libertyville, Ill.-based talent assessment and leadership development training firm that works exclusively with financial services firms.

Dow Jones & Company, Inc.

This information is for your convenience only and IG Wealth Management is not responsible for and disclaims any liability for third-party businesses, organizations and individuals featured in this newsletter. For more information, please visit https://www.investorsgroup.com/en/legal/disclosures.

Jan 08, 2021